The payments industry is evolving to meet the demands of making payment information more secure and transactions more convenient. Businesses, banking entities, payment processors, and payment gateways are expanding their capabilities to accommodate emerging payment technologies. To keep pace with the consumer demand, upgrading the entire infrastructure is paramount to the continued success of players in the payments industry. Software providers have a unique opportunity to offer software platforms that help entities accommodate payment technology trends and ensure that the payments providers are at the forefront of the changes within the market. In 2015 there will be a revolution in the payment industry as it marks a shift toward the use of EMV chip card technology, mobile payments, and cryptocurrencies.

Traditional credit and debit cards are in the process of being phased out and replaced by EMV smart cards, which follow standards set forth by Europay, MasterCard, and Visa (EMV). The cards are the same dimensions as a conventional credit and debit card, but instead of the traditional magnetic stripe, it is equipped with a microprocessor chip. The chip is able to be used more dynamically to validate a transaction, which makes both the card and the transaction more secure. It employs a cryptography and tokenization feature making it far more advanced than a magnetic stripe that can become easily corrupted through use or poor storage. EMV smart cards have a contact function similar to an ATM or a contactless function that uses NFC technology. Although this technology is widely used abroad, it has yet to be implemented in the United States payments infrastructure. However, by October 2015 many major card networks including Visa, MasterCard, AmEx, and Discover are imposing fraud liabilities on parties that do not switch to the new EMV system. FIS reports that over 15 million POS systems and related software need to be augmented, which represents a $6.75 billion market.

Mobile payment technology enables consumers to use mobile devices to execute payment transactions. This is a result of Near-Field Communications (NFC), Quick Response (QR) codes, and cloud-based wallets. To complete payments using NFC capable devices at the Point-Of-Sale (POS), users touch their mobile accessory to a NFC device, and it sends secured payment information to the merchant, finalizing the sale. This hardware technology requires both parties, the buyer and the seller, to have NFC enabled devices. For devices not embedded with NFC hardware, QR codes can be utilized to make payments. Native QR applications are downloaded to a user’s smart device. A barcode matrix made up of black and white squares is generated by the merchant at the POS and the user employs the camera to capture the code. Once captured, the user confirms the payment to complete the payment function. Cloud-based wallets store accounts in a secure virtual cloud. Using Host Card Emulation (HCE) technology a mobile phone can use a contactless function similar to that of an EMV smart card to conduct a payment transaction. An infographic created by mobilepaymentstoday.com explains that in 2015 mobile payments can accumulate up to $1 trillion in transactions.

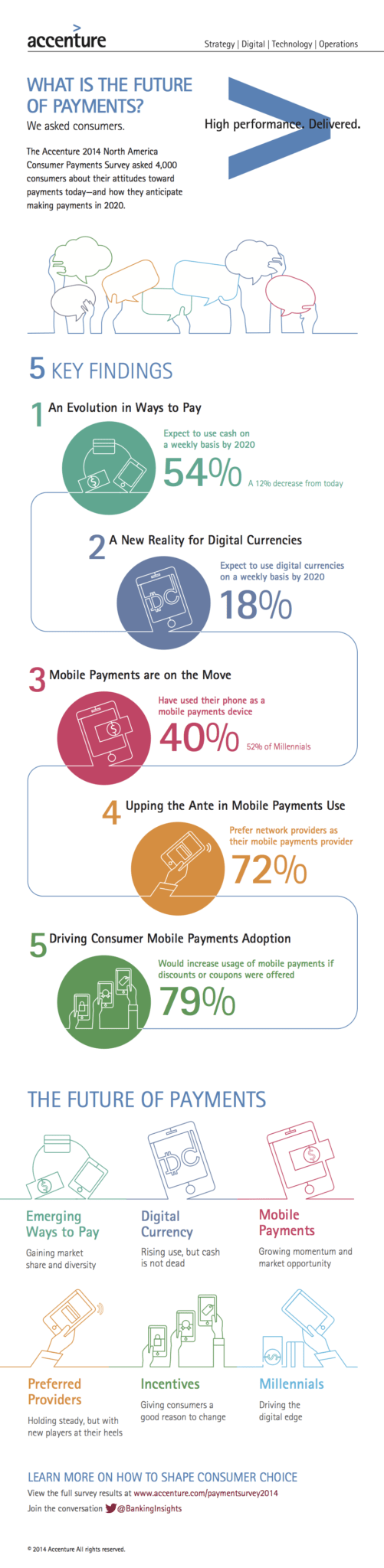

The evolution of standard cash is cryptocurrency; a pairing of customary “flat” money with cryptography to conceive a new monetary system. Cryptocurrencies are a type of digital money that use the latest advances in cryptography as a security measure. Cryptography takes information and transforms it into an unreadable format (encrypting). This information is then passed to the appropriate party who uses a code or key to render this encrypted information readable again (decrypting). Examples of the avant-garde cryptocurrencies available are Bitcoin, Litecoin, and Peercoin. Although smart cards and mobile payments will be primarily used as payment methods, crowdfundinsider.com reports that digital currencies are expected to be used 18% of the time by 2020.

The evolution of standard cash is cryptocurrency; a pairing of customary “flat” money with cryptography to conceive a new monetary system. Cryptocurrencies are a type of digital money that use the latest advances in cryptography as a security measure. Cryptography takes information and transforms it into an unreadable format (encrypting). This information is then passed to the appropriate party who uses a code or key to render this encrypted information readable again (decrypting). Examples of the avant-garde cryptocurrencies available are Bitcoin, Litecoin, and Peercoin. Although smart cards and mobile payments will be primarily used as payment methods, crowdfundinsider.com reports that digital currencies are expected to be used 18% of the time by 2020.

Software providers for payments infrastructure technology must understand the direction of consumer and business interests. It will be imperative for every business big or small to adapt to the new payment technologies. Software providers can be on the ground floor of this development and capitalize on software to alleviate some of the hassles that merchants, retailers, and entities will face when trying to upgrade their payment systems. To accommodate this revolution it will be critical to take into account all the payment technologies that consumers are using. Although the afore mentioned technologies are all different in their own ways, producing all-encompassing payment gateway and payment processing software and hardware, that integrates seamlessly into legacy systems will be a huge selling point. Creating a software that embodies all three of these emerging technologies will be beneficial as businesses are looking to satiate consumer demands. Creating a product that can be smoothly integrated with existing software and hardware will allow retailers to augment their POS while keeping costs minimal.

An entity can develop a loan origination, underwriting, amortization, and document parsing software from scratch to gain market share. This represents an opportunity to create a software that will be tailored to the specific regulations and be able to make an easy-to-use application that maximizes essential workflows. Lenders are looking to cut costs associated with the pre-qualification, origination, and processing procedures while adhering to the CFPB regulations and document formats.

An entity can develop a loan origination, underwriting, amortization, and document parsing software from scratch to gain market share. This represents an opportunity to create a software that will be tailored to the specific regulations and be able to make an easy-to-use application that maximizes essential workflows. Lenders are looking to cut costs associated with the pre-qualification, origination, and processing procedures while adhering to the CFPB regulations and document formats.

Safeguarding Your Online Casino

Safeguarding Your Online Casino

{kind=link}